Harvey Hits 87 AmLaw Firms as BCG Flags Real Estate AI Gap

Slaughter and May and DLA Piper go firmwide on Harvey AI. BCG says real estate invests half the cross-industry average. Healthcare's pilot-to-production rate sits at 8%.

By Springvanta

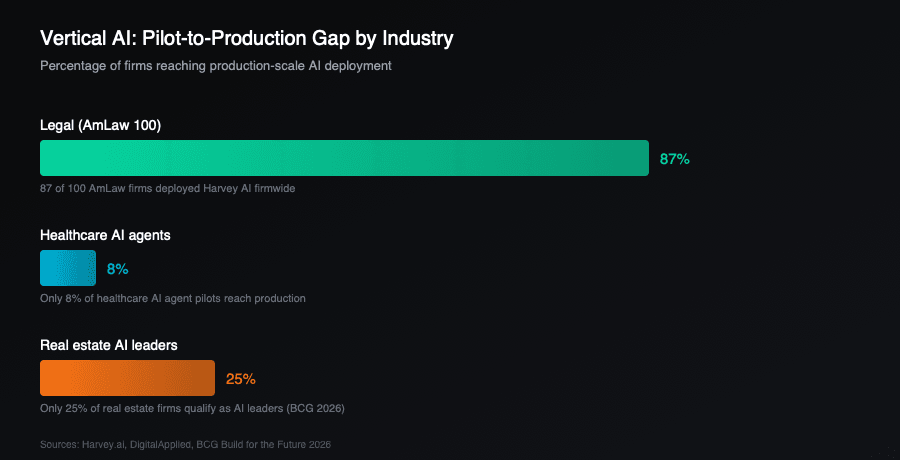

Slaughter and May rolled out Harvey AI across all practice areas on May 1, 2026. DLA Piper expanded to 5,000 licenses. Harvey now serves 87 of the AmLaw 100, up from 42–50% just a year ago. The legal vertical didn't just adopt AI , it standardized on one platform faster than any prior legal technology.

That speed is the story. The enterprise AI agent buying cycle has compressed from 18 months to roughly 8 weeks at the legal tier, according to CallSphere's May 2026 analysis. Two AmLaw 50 firms expanded from pilot to firm-wide rollout in Q2 alone. Harvey's revenue reportedly crossed $100M ARR in late 2025, and the company now employs 781 people across 11 countries.

What changed: security, agents, and the Vault

Harvey's adoption curve accelerated after three product shifts. First, the launch of Vault , isolated client environments that solve attorney-client privilege concerns at scale. Second, Workflow Agents that execute legal work end-to-end rather than just answering queries. Third, the Intapp integration for real-time conflicts checking and ethical wall enforcement, directly addressing one of the biggest barriers to AI adoption in law firms.

Slaughter and May cited Harvey's "security standards, agentic AI capabilities, and experience supporting AI implementation" as the deciding factors. The firm described its lawyers as the "vital human layer" supervising AI-generated work , positioning the technology as augmentation, not replacement.

The cross-vertical gap: legal is ahead, but not alone

Legal's production deployment rate contrasts sharply with other verticals. In healthcare, only 8% of AI agent pilots reach production scale , the lowest of any sector surveyed, per DigitalApplied's March 2026 data. The healthcare voice AI market is growing at a 37.79% CAGR and projected to hit $3.18B by 2030, yet 78% of enterprises with AI agent pilots haven't scaled a single one past the testing phase.

The gap in healthcare comes down to EHR integration depth. Most vendors offer surface-level API connections that read availability but can't write appointments back reliably or handle scheduling conflicts mid-call. Greetmate's May 2026 market analysis notes that 96% of hospitals have adopted FHIR APIs , the technical foundation exists , but most voice AI vendors are still operating at the read-only layer.

Real estate faces a different problem: underinvestment. BCG's May 2026 report on AI-first real estate companies found that only 25% of real estate firms qualify as AI leaders, compared with 40% across all industries. The sector invests roughly half the cross-industry average in AI, lagging even other asset-heavy sectors like utilities. The results are visible: 66% of development projects still finish late, and 39% exceed budget.

BCG's prescription is direct. The firm estimates that an end-to-end AI transformation can deliver 400 to 700 basis points of operating profit improvement for developers. That includes AI-driven pricing and demand forecasting, construction management with measurable safety improvements, and agentic AI embedded into property management workflows for automated maintenance dispatch. The condition: CEO-led action, not scattered pilots.

Why intake workflows sit at the center of all three verticals

The common thread across legal, healthcare, and real estate isn't just AI adoption , it's the first touchpoint where AI meets the customer. Intake.

In legal, Harvey's Vault and Workflow Agents automate conflict checks, matter intake, and document analysis. In healthcare, voice AI agents handle appointment scheduling, insurance verification, and patient demographics capture , the front-desk functions that determine whether a patient becomes a revenue event or a missed call. In real estate, BCG identifies lead analytics and AI-driven demand forecasting as immediate-value use cases, which start with capturing and qualifying inbound inquiries.

The firms that moved first , the 87 AmLaw firms on Harvey, the healthcare groups that hit 50%+ call deflection , treated intake as infrastructure, not a side project. They deployed against a specific operational problem (conflict checks, missed calls, lead qualification) rather than adopting AI as a strategy initiative.

What to watch

Three signals worth tracking through Q3 2026:

- Epic launches 150+ AI features directly into its EHR platform. This raises the integration bar for standalone voice AI vendors and could accelerate the healthcare pilot-to-production rate.

- Managed deployment models are replacing self-serve in healthcare. The 8% production rate is partly a configuration gap , vendors who build and manage the workflow layer are outperforming SaaS licenses that leave setup to the buyer.

- Real estate CEO ownership. BCG reports 72% of CEOs across industries now act as the primary AI decision maker. Real estate's 25% AI leadership rate suggests most firms haven't made that shift yet. The ones that do will have a two-to-three year window before the field catches up.

Sources: Solicitor News (May 1, 2026), Harvey.ai (DLA Piper, Latham & Watkins announcements), CallSphere (May 2026), BCG (May 2026), Greetmate (2026), DigitalApplied (March 2026)